Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

More Buyers Are Planning To Move in 2026. Here’s How to Get Ready.

Momentum is quietly building in the housing market, and that’s something buyers in Rhode Island should watch closely. National trends show an uptick in buyer interest—from 15% of Americans planning to buy in the next 12 months to 17% this year—suggesting confidence is slowly returning to the market. That shift tells us that more people feel ready (or closer to ready) to take the leap and buy a home in 2026.

If buying a home is on your goal sheet this year, now is the time to start laying the groundwork. Early preparation doesn’t rush a decision—it makes your decision more confident and successful.

Rhode Island Market at a Glance

Before we talk strategy, let’s ground you in the current Ocean State market:

-

The median sales price statewide is holding strong near $505,000, up about 5.2% year-over-year, reflecting sustained demand even as transactions have cooled slightly. Rhode Island Association of REALTORS®

-

Inventory remains lean—about 2.3 months of supply—which means well-priced homes still move quickly. Rhode Island Association of REALTORS®

-

In many towns, median sale prices exceed $525,000, and forecasts project moderate price growth of 4–6% through 2026. Real Estate Institute of Rhode Island

-

In Providence/Worcester metro data, median listing prices sit above $550,000—another indicator that buyers need to be ready to act and informed on pricing. FRED

In short: Rhode Island isn’t slowing down on value growth, and buyers can still succeed with the right preparation and strategy.

Planning To Move in Early 2026? Start with These 4 Steps

If your goal is to be active in the first half of 2026, here’s what to tackle now:

1. Get pre-approved.

A pre-approval gives you a real understanding of your buying power and what a monthly payment could look like at today’s rates. Keep in mind that most pre-approvals are only good for 30–90 days, so time this step when you’re close to being ready to act.

2. Run the numbers.

Take a hard look at current expenses and future mortgage costs. With median prices around the $500K range and inventory still limited, you don’t want surprises in the budget once you’re under contract.

3. Define your non-negotiables—and your “nice-tos.”

Know what matters most: town, commute, layout, school districts, and lifestyle. In a competitive Ocean State market, clarity helps you move fast while avoiding regret.

4. Choose your agent early.

Dive into online reviews, talk to a few agents, and connect with someone you trust. The right agent does more than show homes—they guide you through pricing strategy, timing, and negotiation before you ever write an offer.

Thinking About Buying Later in the Year? Now’s Still Your Window To Prepare

Even if late-2026 feels more realistic for your timeline, this moment still matters. The buyers I see feel most confident later are the ones who quietly prepared earlier. Here are low-stress ways to get ready:

Work on your credit.

You don’t need perfect credit to buy—but the stronger your score, the better your loan terms and mortgage rate can be. Consistent payments and reducing debt add up.

Automate your savings.

Set up automatic transfers into your homebuying fund so you’re building consistently without thinking about it.

Lean into your side hustles.

Extra income—freelancing, part-time gigs, seasonal work—can give your savings a significant boost without disrupting your day-to-day life.

Put windfalls to work.

Tax refunds, bonuses, gifts—these are prime opportunities to accelerate your house fund.

The Common Thread? Prep Work Makes a Difference.

Rhode Island’s market isn’t quiet—values are holding and forecasted to continue modest growth in 2026. Getting ready early doesn’t mean rushing a decision; it means you enter the market informed, confident, and strategically positioned.

Bottom Line

If buying a home in 2026 is on your radar, let’s start the conversation now—not to rush anything, but to make sure you’re positioned to win when the right home hits.

This is where my Huard Hustle approach makes the difference: a hands-on, highly guided plan, clear strategy, consistent communication, and fierce advocacy from day one. We’ll map out your timeline, sharpen your buying power, dial in your non-negotiables, and make sure you’re truly ready when it’s game time—because in Rhode Island, the best homes don’t wait.

When you’re ready, I’ll be ready—fully in your corner, every step of the way. Let’s connect and build your 2026 plan.

Reasons To Be Optimistic About the 2026 Housing Market

If a move is on your radar for 2026, there’s a lot to be encouraged about.

After several years when so many felt “stuck,” this year is shaping up to bring balance, momentum, and long-awaited opportunity to both buyers and sellers. Not because real estate suddenly becomes easy—but because the fundamentals are shifting in your favor.

And I’m already seeing it. I listed a home on December 26 and had immediate, back-to-back showing requests before the week was out. Buyers are ready—they’re eager for new, well-priced, and thoughtfully presented inventory. With 12 sellers already lined up for early-2026 launches, the energy is palpable across Rhode Island and Southeastern Massachusetts.

What the Experts Are Saying

-

Danielle Hale, Realtor.com: “After a challenging period for buyers, sellers, and renters, 2026 should offer a welcome, if modest, step toward a healthier housing market.”

-

NAR: “Top economists have one word to sum up the 2026 housing market: opportunity. Lower mortgage rates and rising supply will open up the market—something buyers and sellers have been waiting for.”

-

Mark Fleming, First American: “For the first time in several years, the underlying forces are aligned toward gradual improvement… Affordability won’t snap back overnight, but the ship is sailing in the right direction.”

-

Mischa Fisher, Zillow: “Buyers are benefiting from more inventory and improved affordability, while sellers are seeing price stability and more consistent demand.”

Why Local Insight Matters More Than Ever

While national forecasts are brightening, local dynamics will determine just how opportunity unfolds. Some markets will surge faster than others—and understanding our hyper-local nuances here in Rhode Island and nearby Massachusetts is where strategy matters most.

That’s where my Huard Hustle comes in: deep market knowledge, hands-on guidance, and relentless drive to position my clients for success. I study trends daily, advise on timing and pricing strategy, and collaborate closely on pre-listing preparation so that every property shines from day one.

Bottom Line

2026 is poised to be a year of movement, motivation, and meaningful opportunity. Whether you’re buying or selling, the market is shifting—and it’s moving in your favor.

If you’d like to discuss what these changes mean for your specific neighborhood, your goals, or your next move, let’s connect. I’m here to help you make the most of this promising year—with Huard Hustle + Heart leading the way.

Is January the Best Time to Buy a Home in Rhode Island?

If you’re thinking about buying in Rhode Island, don’t assume you have to wait for spring. While the market feels quieter in winter, January can be a strategic window—especially for buyers who care about value, leverage, and avoiding the peak-season frenzy.

Before we get into the “why,” here’s a quick snapshot of the Rhode Island market backdrop: statewide single-family median sale price was $505,000 in November 2025, with inventory sitting at about a 2.3-month supply (still well below a balanced 5–6 months). Rhode Island Association of REALTORS®

Why January can be a smart move for buyers

1) Pricing tends to be more favorable in winter

A LendingTree analysis points to January as the best month for value nationally, estimating buyers could save roughly $23,400 (for a typical 1,500 sq. ft. home) compared with purchasing during peak demand months. LendingTree

And we see a version of that “winter discount” dynamic locally, too. For example, Rhode Island’s statewide single-family median sales price was $465,000 in January 2025, compared with $480,000 in November 2024 (and $470,000 in December 2024). RILiving

No two years are identical—but seasonal patterns often rhyme, and January routinely brings less heat than late winter into spring.

2) Less competition can mean more negotiating power

Winter typically draws fewer “just browsing” buyers, which can reduce bidding-war intensity and create more room for negotiation. Bankrate summarizes this well: fewer buyers in winter can translate into more leverage for the buyers who are active. Bankrate+1

And across the broader housing market, seller concessions have been meaningful: Redfin data reported by Investopedia found roughly 44% of home sales included seller concessions in Q1 2025 (examples include repair credits or funds for rate buydowns). Investopedia

3) Serious sellers and serious buyers show up in January

In Rhode Island, inventory is still tight overall, which means sellers who list in winter are often doing so with real motivation—and buyers shopping in winter tend to be more decisive. Zillow notes that winter buyers are often motivated by real life changes (relocation, family needs, timing), not just seasonal browsing. Zillow

The Rhode Island reality check: inventory is still low

Even in winter, RI remains a supply-constrained market. For example, in October 2025, RI REALTORS reported inventory that would be exhausted in about 2.8 months at the current sales pace—another signal that good homes can still move quickly even outside spring. Rhode Island Association of REALTORS®

Translation: January can offer better leverage, but it’s not a “slow market” for well-priced, well-presented homes—especially in desirable areas.

What this means if you’re buying in January

A January game plan that wins in Rhode Island usually looks like this:

-

Get fully pre-approved (not just pre-qualified), so you can act decisively when the right home hits.

-

Be ready to negotiate structure, not just price (inspection items, closing timeline, seller credits, rate buydown conversations).

-

Move quickly on the right home—because low inventory means the best options don’t wait around, even in winter.

And if you’re selling: January can be a strong launch point, too

Here’s the seller-side opportunity: fewer competing listings often means your home can stand out more.

Providence metro demand has also been in the spotlight—RI REALTORS noted Realtor.com ranked Providence metro among the top markets for anticipated sales and price gains, pointing to strong demand fundamentals. Rhode Island Association of REALTORS®

My January seller note (important)

I have four listings hitting the market in January, and buyer activity is already underway. If you’re considering a move, now is the time to get me in—so we can build the right pre-listing plan, prep strategically, and position your home to capture eager buyers who are ready to call Rhode Island home.

Bottom line

January can absolutely be one of the best times to buy in Rhode Island—potentially better pricing dynamics, less competition, and more negotiating leverage—as long as you’re prepared to act in a still-low-inventory market.

🔥 The Housing Market “Reset” — What 2026 May Really Look Like 🔥

(Inspired by Redfin’s latest market predictions & a must-watch episode of “On The Market”)

I just finished this powerhouse episode breaking down Redfin’s forecast for a Great Housing Reset in 2026 — and the insights are too important not to share.

Here’s what stood out to me:

📉 Mortgage Rates:

Expect low 6% rates — not the dramatic drops many hope for, but enough to open the door for more movement.

📈 Affordability Slowly Improves:

For the first time in years, home prices are projected to grow more slowly than wages.

This is the start of a long-awaited affordability shift… though the reset could take 5–6 years.

🏡 Sales Will Gently Rise:

Existing home sales may inch from 4.1M → 4.2M, showing cautious confidence returning to the market.

🏘️ Rents Will Creep Up:

With multifamily construction slowing, expect rent pressure in late 2026.

👥 Household Formation Slows:

High costs = more roommates, delayed moves, and quieter household growth.

📜 Affordability Becomes Policy Priority:

We’ll see serious conversations around supply — though local resistance makes change slow.

🔧 Refinance & Renovation Boom:

With rates stabilizing, refi volume could jump 30%, and many homeowners will upgrade rather than uproot.

🌎 Market Winners & Losers:

2026’s hottest markets: NYC suburbs + affordable Midwest metros.

Softer markets: Florida, Texas, and parts of the Sun Belt, influenced by return-to-office trends.

🔥 Climate Migration Quietly Increases:

Within-metro moves driven by climate risk — with insurance premiums as the leading indicator.

🏛️ Industry Reshaping Ahead:

NAR steps back; MLSs step up.

Advocacy becomes the new focus.

🤖 AI Becomes a Real Estate Matchmaker:

Conversational search will help buyers choose where to live and which homes fit their lifestyle.

RI Specific Predictions-

Looking ahead into 2026, the Rhode Island housing market is expected to remain steady and resilient, with home prices projected to grow at a more sustainable 4–6% pace and the statewide median edging toward the $525,000 range. Inventory is showing signs of modest improvement, and paired with easing mortgage-rate pressures, Rhode Island is poised to enter a more balanced market than we’ve seen in years. For buyers, that means slightly less volatility and more strategic opportunity; for sellers, well-priced, well-prepared homes will continue to shine in a landscape where demand still outpaces supply. And this is exactly where expert guidance matters. As a former Brown University varsity athlete, I bring a competitive edge and relentless drive to every transaction. As a former Brookline, MA teacher, I deliver a deeply thorough, detailed, and guided approach that ensures every client feels informed, empowered, and supported from start to finish. If you’re considering a move in 2026, let’s strategize together — with grit, precision, and the Huard Hustle working entirely in your favor.

Bottom Line:

There’s no crash coming — just a slow, steady reset that brings the market back into balance.

As someone immersed in the RI & Southeastern MA markets every single day, this aligns with so much of what I’m experiencing on the ground with buyers, sellers, and homeowners preparing for their next chapter.

If you’re wondering how these trends might shape your 2026 move, I’m here to guide you with the Huard Hustle + Heart. 💙🏡

Why Buying a Home Still Pays Off in the Long Run

By Sarah Huard – RI & Southeastern MA Realtor, Mott & Chace Sotheby’s International Realty

Renting can feel easier. No repairs. No taxes. No stress over interest rates. You simply pay the bill each month and move on with your life.

But here’s the truth I see every day in my work across Rhode Island and Southeastern Massachusetts: renting may be simpler in the moment, but it doesn’t build your future. Homeownership does.

As someone who has helped more than 30 buyers and sellers already this year—across Barrington, Providence, Bristol, Narragansett, Warren, Cumberland, Seekonk, and beyond—I can tell you with certainty: the long-term financial impact of owning a home is profound.

Let’s break it down.

Renting vs. Owning: What Really Happens Over Time

When you rent, your entire payment disappears into your landlord’s pocket. Month after month, year after year.

When you buy, part of every mortgage payment comes back to you in the form of equity—the wealth you build as your home increases in value and your loan balance decreases. That equity becomes leverage, stability, and long-term security. It becomes your next home, your child’s college fund, or part of your retirement.

A recent study from First American compared the true financial outcomes of renting versus owning across several key market periods:

-

2006 (the housing bubble)

-

2015

-

2019 (pre-pandemic)

-

2022 (when rates spiked)

Across every timeline, one thing remained constant:

➡️ Renters lost money over time.

➡️ Homeowners gained it.

Even after factoring in taxes, maintenance, insurance, and repairs, owners still came out dramatically ahead.

Why?

Because time in a home builds wealth. Time renting does not.

It’s that simple.

Real Talk from the Rhode Island Market

Here in RI and nearby MA, I’ve watched this play out over and over. A buyer who purchased in Barrington, Rumford, or Seekonk just 3–5 years ago is often sitting on six-figure equity today. Even condo buyers in Providence and Warwick have seen impressive growth.

Meanwhile, renters in those same communities are paying higher rents each year with no long-term return.

Your home is more than where you live—it’s a powerful financial tool. And in our market, that tool has historically performed incredibly well.

“But Sarah… buying still feels impossible right now.”

Totally understandable.

The past few years have been tough for buyers. But the landscape is quietly shifting:

-

Mortgage rates have come down from their peak

-

Home prices are softening in several RI towns

-

Household incomes have risen

-

Typical monthly payments are improving, according to Zillow

-

More homes are hitting the market compared to last year

Is buying “easy”? Not yet.

Is it easier than it was even a few months ago? Yes.

And in the long run—especially in markets like ours—buying remains one of the most strategic financial moves you can make.

The Bottom Line

Renting may feel less expensive today, but it does nothing for tomorrow. Homeownership builds wealth—consistently, predictably, and powerfully over time.

If you’re curious about what buying could look like for you, I’m here to walk you through it with zero pressure—just expertise, local insight, and my signature Huard Hustle + Heart.

Let’s explore your options.

Your future self will thank you.

The Top 2 Things Rhode Island Homeowners Need To Know Before Selling

By Sarah Huard, REALTOR® | Mott & Chace Sotheby’s International Realty

If you’re thinking about selling your home in Rhode Island—or in nearby Southeastern Massachusetts—here’s something important to know:

The sellers who win in today’s market aren’t the ones waiting on the sidelines. They’re the ones who adapt from the start.

This year, a number of homeowners didn’t get the outcomes they hoped for. But it wasn’t because the market was “off.”

It’s because their expectations were.

Nationwide, Realtor.com reports 57% more homes were pulled off the market compared to last year—meaning they listed but didn’t sell. I see the same patterns here in Rhode Island, especially among sellers who weren’t guided with clarity or strategy from day one.

As someone who has already closed 30 transactions this year, representing over $23 million in sales volume, I have my hands—and my heart—deep in the market every single day. That level of activity provides a real-time pulse on buyer behavior, pricing shifts, neighborhood trends, and what truly drives offers in today’s landscape.

And the truth is simple: the listings that stalled this year almost always came down to price and timing.

Both are entirely fixable—with the right strategy.

Here’s what you need to know so you don’t fall into the traps that derailed so many other sellers.

1. Price It Right from Day One

Pricing is the single biggest driver of a successful sale.

Today, 8 in 10 sellers expect to get their asking price or more, yet only 1 in 4 actually do (Redfin). Why?

Because many are still anchored to 2021 expectations.

What’s happening in Rhode Island right now?

Across Barrington, Bristol, Warren, Providence, East Providence, Cumberland, Tiverton, and more, buyers are:

-

More selective

-

More informed

-

Less willing to pursue an overpriced home

Inventory has increased just enough to give buyers choices—meaning the “list high and wait” strategy simply doesn’t work anymore.

HousingWire notes the average price reduction nationally is just 4%.

But many RI sellers listed even higher, panicked when demand didn’t materialize immediately, and took their homes off the market instead of making that small, strategic adjustment.

Had they priced correctly from day one—or adjusted early—they likely would have sold.

What my volume means for your sale

With over $23M in closed volume this year, I’m in living rooms, at inspections, analyzing comps, and negotiating offers across the state weekly.

I know exactly how buyers are responding at each price point because I’m in the field every day—not watching from afar.

Smart, data-backed pricing isn’t about going lower.

It’s about positioning your home to command strong attention and protect your equity.

2. Don’t Rush the Process

The second major misconception:

Expecting your home to sell instantly.

Many sellers still remember the lightning-fast pace of 2020–2021. But that was an anomaly.

Today, a normalized RI market looks like:

-

30–60 days from list to accepted offer

-

Steady, intentional buyer activity

-

Thoughtful decision-making, not frenzy

It feels slower only because we’re comparing it to a once-in-a-lifetime market.

Think of it as shifting from 70 mph to 35 mph—you’re moving at the right speed for the conditions, even if it feels different.

Where the Huard Hustle makes the difference

If you want your home to sell efficiently and competitively, strategy matters more than ever:

-

Comprehensive pre-listing prep (a cornerstone of my service)

-

Staging and styling that meets today’s buyer expectations

-

Magazine-quality photography + video

-

Precision pricing grounded in hyperlocal data

-

Hands-on, proactive guidance from an agent deeply active across all RI price points

With 30 successful closings so far this year, I’ve seen firsthand:

The homes that sold quickly weren’t just beautiful—they were positioned right.

Bottom Line

The listings that didn’t sell this year weren’t doomed.

They simply started with the wrong expectations and strategy.

In today’s Rhode Island and Southeastern MA markets, success comes from:

-

Strategic, data-backed pricing

-

Patience and understanding of today’s timeline

-

Partnering with a local agent with depth, experience, and relentless advocacy

With 30 transactions and over $23 million in volume this year, I bring unmatched market insight—and the Huard Hustle—to ensure your home is positioned to win from day one.

You can succeed in this market.

You just need the right plan—and the right partner.

Thinking about selling?

Let’s talk value, timing, and strategy. I’d be honored to guide you.

Rhode Island Home Equity: Why You’re still way ahead

Why Your Home Equity Still Puts You Way Ahead

If you’ve seen headlines about home prices dipping, it’s easy to wonder what that means for your home’s value. The truth? Even with minor fluctuations, Rhode Island homeowners are still far ahead—thanks to the incredible equity growth of the past several years.

The Connection Between Home Prices and Equity

Home equity moves hand in hand with home prices. When prices rise, equity builds. When they cool slightly, equity growth slows—but rarely reverses.

Here’s what that looks like locally.

After the record-breaking surge in home prices during 2020 and 2021, a cooling period was inevitable. Back then, Rhode Island’s housing inventory reached historic lows, driving intense buyer competition across Barrington, Bristol, Providence, and beyond. Prices soared—and so did equity.

Now, as inventory inches upward and the market rebalances, prices have leveled—but homeowners remain in a very strong position. In my own experience closing 30 transactions so far this year throughout Rhode Island and Southeastern Massachusetts, I’ve seen firsthand how sustained equity gains are empowering homeowners—whether they’re upsizing, downsizing, or relocating.

Putting It into Perspective

According to Zillow, home prices have risen roughly 45% nationwide since March 2020. Here in Rhode Island, the median sale price has increased approximately 40% in that same period, depending on the community.

Even in areas where prices have softened slightly, those changes are minimal—typically in the 2–4% range—and they don’t come close to erasing the substantial equity homeowners have built over the past five years.

In other words, the sky isn’t falling. It’s stabilizing. And after several years of record-breaking appreciation, Rhode Islanders are still sitting on historic equity.

What That Means for You

If you’ve owned your home for even a few years, odds are you’ve built meaningful wealth—equity that can help you make your next move confidently. Whether you’re considering:

-

Upsizing to meet growing family needs

-

Downsizing to simplify and unlock cash flow

-

Investing in another property or renovation project

…your equity gives you options.

And if you’re unsure what your current home is worth, you may be pleasantly surprised. Across my Rhode Island and Southeastern Massachusetts sales this year, homeowners who hadn’t tracked their property value closely were shocked—in a good way—by how much equity they’d gained.

The Market Is Balancing—Not Breaking

As Realtor.com’s Senior Economist Jake Krimmel notes:

“The slight recent declines in aggregate value and total home equity are not cause for concern… large price declines nationally are extremely unlikely in the near term.”

This moderation is a healthy sign—a recalibration after years of unsustainable growth. Homeowners remain in an enviable position, especially in Rhode Island, where limited inventory and steady demand continue to support strong home values.

Bottom Line

Even with some price adjustments, today’s Rhode Island homeowners are still well ahead.

If you’re curious about how much equity you’ve built—or how to leverage it for your next move—let’s connect. With over 30 transactions closed so far this year and an intimate pulse on the Rhode Island and Southeastern Massachusetts markets, I can help you determine your home’s true market position and plan your next steps strategically.

You might be surprised by how much your home is worth—and how far ahead you really are.

Common Home Inspection Issues in Rhode Island: What Buyers Should Know

Buying a home in Rhode Island (or nearby southeastern Massachusetts) means falling in love with charming properties that often come with a bit of history—and sometimes, a few quirks revealed during a home inspection. I always tell my buyers: inspections aren’t about finding a “perfect” home; they’re about understanding the one you’re buying so you can make confident, informed decisions. And that’s where having a hyper-local expert in your corner makes all the difference.

Here in RI, moisture tops the list of common findings. We live in a coastal, high-water-table state with humid summers and heavy spring rains. It’s extremely common to see evidence of past or minor water incidents in basements. In fact, I’ve yet to meet a home that hasn’t been affected by our historic 2010 flooding in some way.

The good news? Many water-related findings are easily resolved with simple exterior fixes—cleaning gutters, improving grading, or installing properly sized downspouts. At one point, we began noticing water in our own basement and feared the worst. After consulting with a few local basement waterproofing companies, we learned all we needed was a new downspout! A simple fix that made all the difference.

It’s also perfectly normal to see one or two dehumidifiers running in basements across Rhode Island. I run two myself, 365 days a year. In our climate, proactive moisture management isn’t a red flag—it’s responsible homeownership.

Another frequent note is radon. Radon mitigation systems are common throughout the region and relatively straightforward to install. A flagged test result isn’t cause for alarm—it’s simply something to plan for and address.

Beyond that, you’ll often see standard maintenance items: missing GFCI outlets, aging mechanicals, minor exterior wood rot, or handrail updates. These are part of regular homeownership, not deal-breakers.

My role as your Realtor is to help you distinguish between “typical for Rhode Island” and “worth negotiating.” After walking hundreds of inspections, I know what’s normal, what’s worth addressing, and which local pros to call when needed.

When you work with me, I’ll prepare you for what we’re likely to see before we even make an offer—so when that inspection report lands, you’ll be informed, calm, and confident. That’s the Huard Hustle in action: bringing expertise, perspective, and peace of mind to every step of your journey home.

Thinking of buying in Rhode Island or Southeastern Massachusetts? Let’s connect to talk about how to navigate inspections with confidence—and find a home that feels like the perfect fit. I’d love to guide you with the same grit, heart, and local expertise that define the Huard Hustle.

Why Some Homes Sell Quickly- and Others Don’t Sell at All

Why Some Homes Sell Quickly – and Others Don’t Sell at All

Why are some homes selling while others sit—especially now that more listings are hitting the market?

The difference isn’t luck. It’s strategy.

With more inventory and discerning buyers, the homes that stand out are those priced precisely, prepped intentionally, and marketed strategically from day one.

That’s exactly what my Huard Hustle approach is all about—bringing grit, heart, and relentless preparation to help my clients launch with luster and sell with success.

If a move is on your horizon, now’s the time to start planning your strategy. Let’s connect and put the Huard Hustle to work for you—no pressure, just trusted guidance rooted in results. Check out the information below on home movement or lack thereof , on a national level.

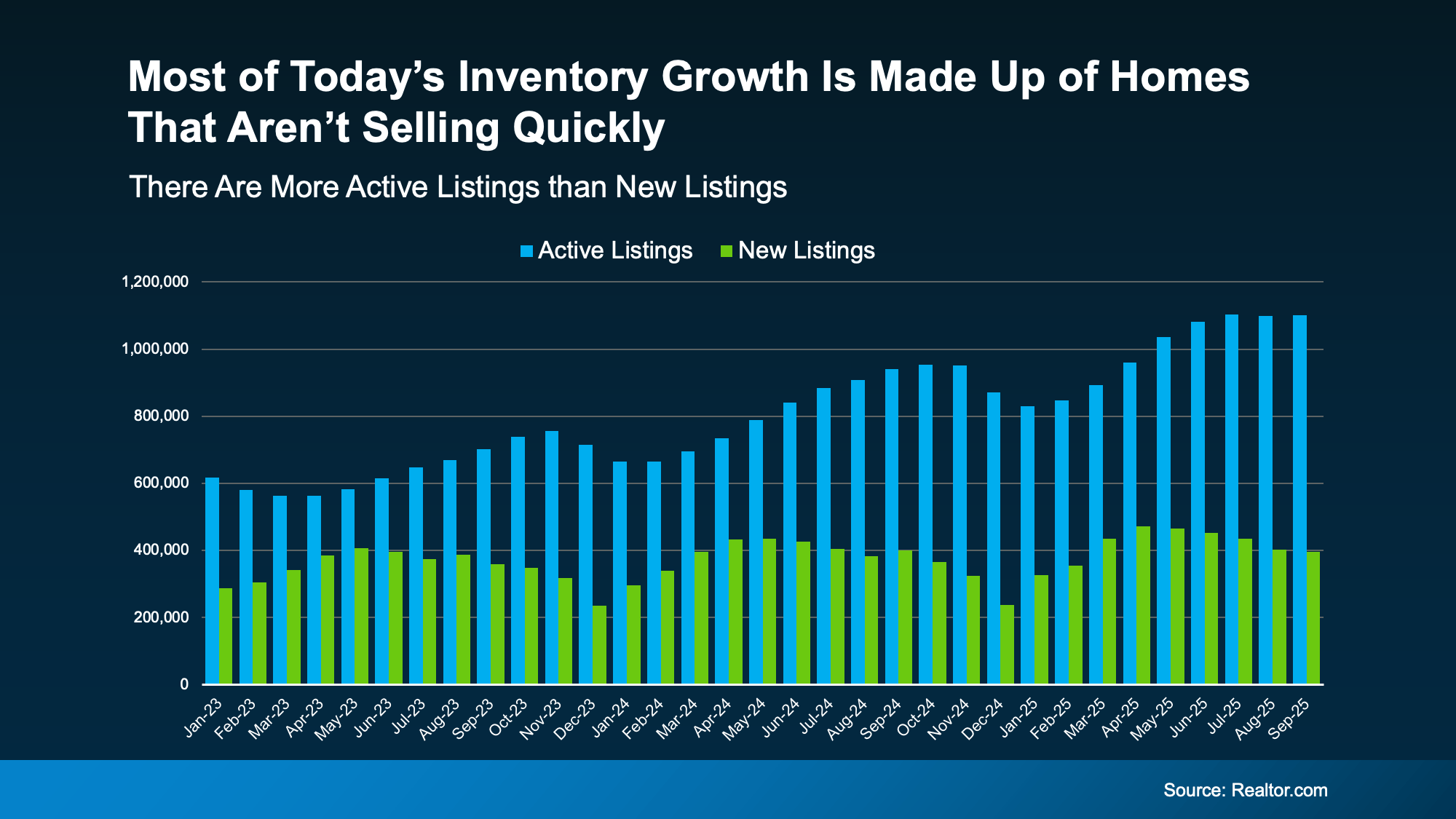

A few years ago, inventory hit a record low. Just about anything sold – and fast. But now, there are far more homes on the market. Listings are up almost 20% from this time last year. And in some areas, supply is even back to levels we last saw in 2017–2019. For sellers, that means one thing:

Your house needs to stand out and grab attention from day one.

That’s especially true when you consider why the number of homes for sale is up. Here’s how it works. Available inventory is a mix of:

- Active Listings: homes that have been sitting on the market, but haven’t sold yet

- New Listings: homes that were just put on the market

Data from Realtor.com shows most of the inventory growth lately is actually from active listings that are staying on the market and taking longer to sell (see the graph below).

The blue bars show active listings. These are the homes that are sitting month to month and not selling. The green bars are new listings, the homes that were just put on the market. And it’s clear there are fewer new listings compared to how many are staying on the market unsold.

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

Why Some Homes Sell and Others Sit

The secret to selling in today’s market is simple. Make sure your house is easy for buyers to say yes to as soon as it is listed.

Price it based on current conditions (not what your neighbor sold for 3 years ago). Make important repairs. And highlight the best things about your house. If you do that, it will sell in any market – sometimes even faster than you’d think. Because the truth is, homes that are priced right today are still selling.

It’s the homeowners who are clinging to outdated expectations that are seeing their house sit and their listing go stale. According to Redfin and HousingWire, here are some of the most common reasons sales stall out:

- Priced it too high from the start

- Skipped necessary repairs before listing

- Didn’t stage the house well

- Sellers won’t negotiate with buyers

- Limited availability for showings

- Ineffective marketing or listing pictures

Most of those things didn’t matter as much just a few years ago. When inventory was at a record low, sellers could skip the prep, name their price, and still walk away with multiple offers over their asking price.

But today’s market is different now that inventory has grown. And that means your approach needs to be different too.

You don’t want to try out old strategies and aim too high just to see what sticks. Your first few weeks on the market are everything. That’s when your listing gets the most attention – and when pricing or presentation mistakes hurt the most. Get it wrong up front and your house will sit…and sit. Get it right, and it’ll be snatched up before you know it.

The Right Agent Helps Your House Stand Out

Selling quickly isn’t about luck. It’s about knowing how to play to the market you’re in. And that’s where your agent comes in.

A great agent will analyze your local market, suggest a price based on the latest comparables sold in your neighborhood, and create a marketing plan that makes buyers pay attention from day one. They’ll also walk you through any repairs you need to make or whether you need to bring in a staging company. As the National Association of Realtors (NAR) explains:

“Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home.”

That’s the power of getting it right (and getting expert help) from the start.

Bottom Line

There are more homes for sale today than there were even just a year ago, but that doesn’t have to work against you.

When your house is priced right, shows well, and is marketed effectively, it will sell. Let’s connect if you want to know how to make that happen in our market this fall.