Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

August Market News & Message

|

Thinking of buying a home? Here are some of Sarah’s Tips to Guide You!

Hi there, future homeowner! If you’re reading this, you’re probably toying with the idea of buying your first home. It’s exciting, nerve-wracking, and a bit overwhelming. But don’t worry, I’ve got you covered. Think of this as your trusty guide to navigating the wild world of real estate in Rhode Island.

By the end of this post, you’ll be well on your way to making that dream home a reality. Plus, I’ve got something special for you – a free home buyer guide that’ll be your game-day playing card throughout this journey. Ready? Let’s dive in!

1. Understanding Your Budget: More Than Just a Number Before you start touring homes or even scrolling through listings, it’s crucial to understand your budget. This isn’t just about knowing how much you can spend; it’s about knowing what you can comfortably afford.

Here’s how to get started:

Assess Your Finances: Look at your income, savings, and current expenses. What’s your monthly net income after taxes? How much are you saving, and what can you afford to put toward a mortgage each month?

Check Your Credit Score: Your credit score plays a big role in the mortgage rates you’ll be offered. The higher your score, the better the rates.

Get Pre-Approved: This gives you a clear picture of what you can afford and shows sellers you’re serious. Plus, it makes the whole process smoother and quicker. Pro Tip: Download our free home buyer guide for a detailed breakdown of budgeting tips and a handy checklist to keep you on track!

2. Finding the Right Neighborhood: Location, Location, Location Finding the perfect home isn’t just about the house itself – it’s also about the neighborhood. You should consider

Safety First: Check out crime rates and talk to locals about how safe they feel.

School Districts: Good schools can increase your home’s value even if you don’t have kids.

Amenities: What’s nearby? Grocery stores, parks, coffee shops? Make sure the neighborhood fits your lifestyle.

Commute: How long will it take you to get to work? Consider traffic patterns and public transportation options.

3. The House Hunt: What to Look For in a Home Now, the fun part – house hunting! Here’s how to make the most of it:

Make a Must-Have List: What are your non-negotiables? A big kitchen, a backyard, or maybe a home office?

Be Open-Minded: Finding a home that ticks every box is rare. Be prepared to compromise on some aspects.

Check the Bones: Pay attention to the structure and condition of the house. Look for signs of wear and tear, and don’t be afraid to ask about the age of the roof, plumbing, and electrical systems.

Consider Future Value: Consider how the home’s value might increase over time. Are there plans for new developments in the area? Is the neighborhood up-and-coming?

Freebie Alert: Our home buyer guide includes a comprehensive checklist to take with you on house tours, ensuring you don’t miss a thing!

4. Making an Offer: The Art of Negotiation You’ve found the one – now what? Making an offer can be nerve-wracking, but here’s how to navigate it:

Do your research: Know the market value of similar homes in the area. I will provide you with a solid understanding of the market values around the home you seek, giving you a solid foundation for your offer.

Be Prepared to Negotiate: Sellers often list their homes as being higher than what they expect to get. Don’t be afraid to make a counteroffer. Include Contingencies: Protect yourself with financing, inspections, and appraisal contingencies.

Stay Calm: It’s easy to get emotionally attached, but stay level-headed. If this one doesn’t work out, there’s always another home out there. Download Now: I have a “How to write a competitive offer” PDF I’d happily share once we find the house you want to compete for. It has detailed strategies for making offers and negotiating like a pro.

5. Closing the Deal: From Offer to Ownership Closing is the final step, and it involves paperwork.

Here’s what to expect:

Home Inspection: Ensure the home is in good condition. If issues are found, negotiate repairs or a price reduction.

Appraisal: The lender will require an appraisal to confirm the home’s value.

Final Walkthrough: Do one last check to ensure everything is in order. Closing Costs: Be prepared for additional costs, including lender fees, title insurance, and property taxes.

Signing the Papers: Finally, you’ll sign the documents, transfer the funds, and get the keys to your new home.

To Wrap Up, Buying your first home is a big step, but with the right preparation and guidance, you can navigate it confidently. Remember to stay flexible, keep an open mind, and don’t hesitate to ask for help. And speaking of help, don’t hesitate to contact me if you’d like my custom home buyer guide – it’s packed with all the tips, checklists, and advice you need to make your home-buying journey as smooth as possible. Happy house hunting, and welcome to the next exciting chapter of your life! I am here to help with Huard Heart + Hustle!

Thinking of buying a condo? Here are some key factors to consider

𝐍𝐚𝐯𝐢𝐠𝐚𝐭𝐢𝐧𝐠 𝐘𝐨𝐮𝐫 𝐅𝐢𝐫𝐬𝐭 𝐂𝐨𝐧𝐝𝐨 𝐏𝐮𝐫𝐜𝐡𝐚𝐬𝐞: 𝐊𝐞𝐲 𝐅𝐚𝐜𝐭𝐨𝐫𝐬 𝐭𝐨 𝐜𝐨𝐧𝐬𝐢𝐝𝐞𝐫

Owning a home is a significant milestone, and for many first-time buyers, condominiums present an appealing option. The allure of shared amenities, lower maintenance responsibilities, and potential cost savings can make condos an attractive choice. However, before diving into this exciting venture, it’s crucial to consider several factors to ensure a well-informed decision. I am active in the condo resale market in Rhode Island and am happy to offer some key points to consider when looking at buying a condo!

1. Location Matters:

Proximity to work, public transportation, shopping, and essential services should top your priority list. Assess the neighborhood’s safety, future development plans, and overall livability.

2. Condo Association Rules and Fees:

Understand the rules and regulations of the condominium association. Examine monthly fees, what they cover, and if there’s a reserve fund for major repairs. This will impact your budget and lifestyle.

3. Financial Readiness:

Evaluate your financial health and ensure you’re ready for homeownership. Consider your credit score, existing debts, and future earning potential—factor in the purchase price, closing costs, property taxes, and homeowner’s insurance.

4. Resale Value:

Investigate the resale value of similar units in the condo complex. A real estate investment should ideally appreciate over time, so understanding the market trends can help you make a more informed decision.

5. Amenities and Community Atmosphere:

Condos often have shared amenities like gyms, pools, or communal spaces. Assess whether these align with your lifestyle. Additionally, attend community events or meetings to gauge the atmosphere and sense of community within the condominium.

6. Building Maintenance and Condition:

Inspect the overall condition of the building, common areas, and individual units. Who manages the property? Are snow removal and ground maintenance covered? Understanding the maintenance schedule and any upcoming renovations is crucial for long-term satisfaction.

7. Reserve Fund:

A well-funded reserve is vital for covering unexpected repairs or improvements. Lack of financial planning in the condo association may result in special assessments for homeowners, potentially affecting your budget.

8. Rental Policies:

If there’s a possibility you might need to relocate in the future, familiarize yourself with the condo’s rental policies.

9. Future Development Plans:

Research any planned developments in the area that may impact your condo’s value or quality of life.

10. Legal Review:

Engage a real estate attorney to review the condo’s legal documents, including the association’s bylaws, covenants, conditions, and restrictions (CC&Rs).I have some great attorneys to recommend!

If you are considering buying a condo in RI or Southern MA and seeking guidance, reach out! I am here to help!

What You Should Know About Closing Costs

As I help one buyer make an offer and close on another home with a seller today, closing costs are the theme of the day!

Before you buy a home, it’s essential to plan ahead. While most buyers consider how much they need to save for a down payment, many are surprised by the closing costs they have to pay. To ensure you aren’t caught off guard when it’s time to close on your home, you need to understand what closing costs are and how much you should budget for.

What Are Closing Costs?

People are sometimes surprised by closing costs because they don’t know what they are. According to Bankrate:

“Closing costs are the fees and expenses you must pay before becoming the legal owner of a house, condo or townhome . . . Closing costs vary depending on the purchase price of the home and how it’s being financed . . .”

In other words, your closing costs are a collection of fees and payments involved with your transaction. According to Freddie Mac, while they can vary by location and situation, closing costs typically include the following:

- Government recording costs

- Appraisal fees

- Credit report fees

- Lender origination fees

- Title services

- Tax service fees

- Survey fees

- Attorney fees

- Underwriting Fees

How Much Will You Need To Budget for Closing Costs?

Understanding closing costs is essential, but knowing what you’ll need to budget to cover them is also critical. According to the Freddie Mac article mentioned above, the costs to close are typically between 2% and 5% of the total purchase price of your home. With that in mind, here’s how you can get an idea of what you’ll need to cover your closing costs.

Let’s say you find a home you want to purchase for the median price of $366,900. Based on the 2-5% Freddie Mac estimate, your closing fees could be roughly $7,500 and $18,500.

If you’re in the market for a home above or below this price range, your closing costs will be higher or lower.

What’s the Best Way To Make Sure You’re Prepared at Closing Time?

Freddie Mac provides excellent advice for homebuyers, saying:

“As you start your homebuying journey, take the time to get a sense of all costs involved – from your down payment to closing costs.”

Work with a team of trusted real estate professionals to understand exactly how much you’ll need to budget for closing costs. An agent can help connect you with a lender, and your expert team can answer any questions.

Bottom Line

It’s important to plan for the fees and payments you’ll be responsible for at closing. Let’s connect so I can help you feel confident throughout the process. Helping others is my “why I’m here” part!!!

What Are Your Real Estate Goals This Year?

If buying or selling a home is part of your dreams for 2023, it’s essential for you to understand today’s housing market, define your goals, and work with industry experts to bring your homeownership vision for the new year into focus.

In the last year, high inflation greatly impacted the economy, the housing market, and your wallet. That’s why it’s critical to clearly understand not just the market today but also what you want out of it when you buy or sell a home. Danielle Hale, Chief Economist at realtor.com, explains:

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, so that you can stay in your home long enough that buying is a sound financial decision.”

Here are a few questions you can start thinking through as you fine tune your goals for 2023.

1. What’s Motivating You?

You’re dreaming about making a move for a reason – what is it? No matter what’s happening in the market, there are many compelling reasons to buy a home today. Your needs may have changed in a way your current house can’t address, or you could be ready to step into homeownership for the first time and have a space that’s your own. Use what’s motivating you as a guidepost in partnership with an expert advisor to help make sure your move will give you a lasting sense of accomplishment.

2. What Does Your Next Home Look Like?

You know you want to move, but how would you describe your dream home? The available supply of homes for sale has grown, which could mean more options to choose from when you buy. Just be sure to keep your budget in mind and work with a trusted real estate professional to balance your wants and needs. The better you understand what’s essential and where you can be flexible, the easier it can be to find the right home for you.

3. How Ready Are You To Buy?

Getting clear on your budget and savings is essential before you get too far into the process. Working with a local agent and a lender early is the best way to ensure you’re in a good position to buy. This could include planning how much to save for a down payment, getting pre-approved for a home loan, and assessing your current home equity if your move involves selling your existing house.

A Professional Will Guide You Through Every Step of the Process

Buying or selling a home is a big process that takes expertise to navigate. If that feels a bit overwhelming, you aren’t alone. According to a recent Harris Poll survey, one in five respondents sees a lack of information or knowledge about the home-buying process as a barrier to owning a home. Don’t let uncertainty hold you back from your goals this year. A trusted expert can bridge that gap and give you the best advice and information about today’s market.

Bottom Line

If your 2023 plans entail buying or selling in MA or RI, let’s connect to plan how your dreams for 2023 can become a reality. Helping my clients is why I am here!

What Every Seller Should Know About Home Prices

If you’re trying to decide whether or not to sell your house, recent headlines about home prices may be top of mind. And if those stories have you wondering what that means for your home’s value, here’s what you need to know.

What’s Happening with Home Prices?

You may have seen news stories mentioning a drop in home values or home price depreciation, but it’s important to remember those headlines are designed to make a big impression in just a few words. But what headlines aren’t always great at is painting the full picture.

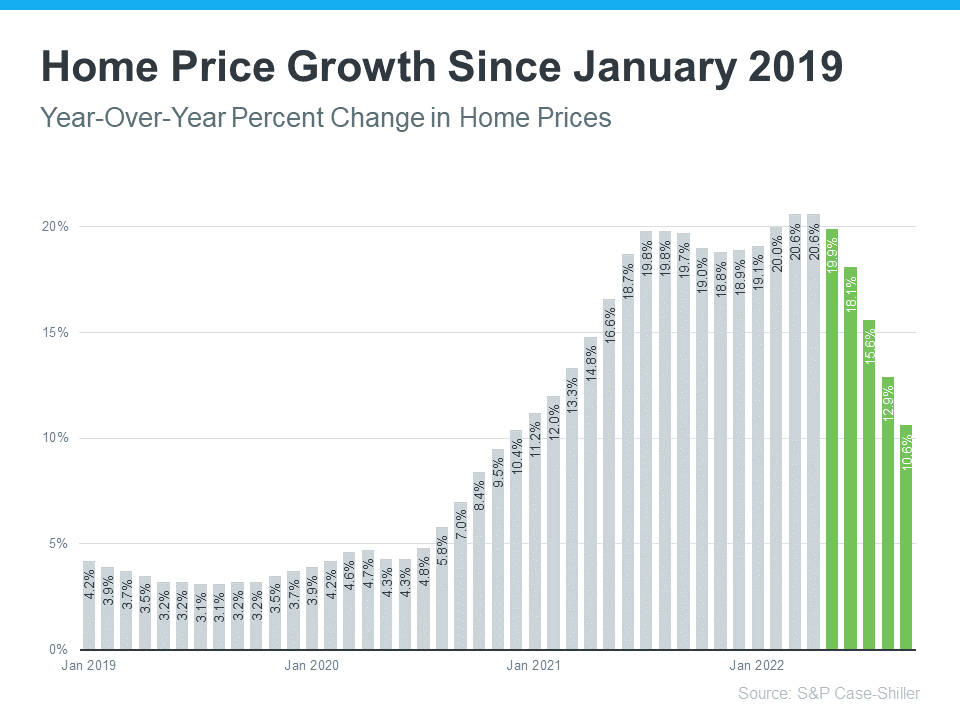

While home prices are down slightly month-over-month in some markets, it’s also true that home values are up nationally on a year-over-year basis. The graph below uses the latest data from S&P Case-Shiller to help tell the story of what’s happening in the housing market today:

As the graph shows, home price growth has moderated in recent months (shown in green) as buyer demand has pulled back in response to higher mortgage rates. This is what the headlines are drawing attention to today.

But what’s important to notice is the bigger, longer-term picture. While home price growth is moderating month-over-month, the percent of appreciation year-over-year is still well above the home price change we saw during more normal years in the market.

The bars for January 2019 through mid-2020 show that home price appreciation of around 3-4% a year was more typical (see bars for January 2019 through mid-2020). But even the latest data for this year shows prices have still climbed by roughly 10% over last year. Last week’s RI Market Report for single-family homes shows an increase of 9.7% in the median sale price for November 2022 compared to one year prior.

What Does This Mean for Your Home’s Equity?

While you may not be able to capitalize on the 20% appreciation we saw in early 2022, in most markets, your home’s value, on average, is up 10% over last year – and a 10% gain is still dramatic compared to a more normal level of appreciation (3-4%).

The big takeaway? Don’t let the headlines hinder your plans to sell. Over the past two years alone, you’ve likely gained a substantial amount of equity in your home as home prices climbed. Even though home price moderation will vary by market moving forward, you can still use the boost your equity got to help power your move.

As Mark Fleming, Chief Economist at First American, says:

“Potential home sellers gained significant amounts of equity over the pandemic, so even as affordability-constrained buyer demand spurs price declines in some markets, potential sellers are unlikely to lose all that they have gained.”

Bottom Line

If you have questions about home prices or how much equity you have in your current Rhode Island or Massachusetts home, let’s connect so you have an expert’s advice. I am here to help!

Top Questions About Selling Your Home This Winter

There’s no denying the housing market is undergoing a shift this season, which may leave you with questions about whether it still makes sense to sell your house. Here are three of the top questions you may be asking – and the data that helps answer them – so you can make a confident decision.

1. Should I Wait To Sell?

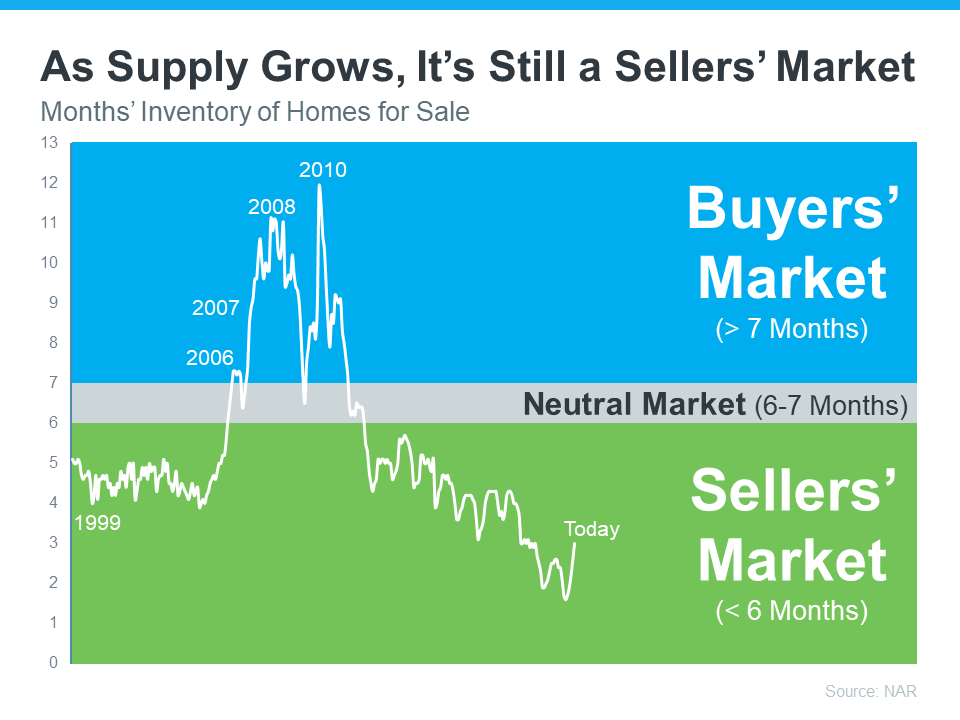

Even though the supply of homes for sale has increased in 2022, inventory is still low overall. That means it’s still a sellers’ market. The graph below helps put the inventory growth into perspective. Using data from the National Association of Realtors (NAR), it shows just how far off we are from flipping to a buyers’ market:

While buyers have regained some negotiation power as inventory has grown, you haven’t missed your window to sell. Your house could still stand out since inventory is low, especially if you list now while other sellers hold off until after the holiday rush and the start of the new year. Home prices were up 8.8% year-over-year in October here in RI. The median sale price in RI stands strong at $46,500, and the number of homes for sale in RI is down a whopping 23.8%.

2. Are Buyers Still Out There?

If you’re thinking of selling your house but are hesitant because you’re worried buyer demand has disappeared in the face of higher mortgage rates, know that isn’t the case for everyone. While demand has eased this year, millennials are still looking for homes. As an article in Forbes explains:

“At about 80 million strong, millennials currently make up the largest share of homebuyers (43%) in the U.S., according to a recent National Association of Realtors (NAR) report. Simply due to their numbers and eagerness to become homeowners, this cohort is quite literally shaping the next frontier of the homebuying process. Once known as the ‘rent generation,’ millennials have proven to be savvy buyers who are quite nimble in their quest to own real estate. In fact, I don’t think it’s a stretch to say they are the key to the overall health and stability of the current housing industry.”

While the millennial generation has been dubbed the renter generation, that namesake may not be appropriate anymore. Millennials, the largest generation, are actually a significant driving force for buyer demand in the housing market today. If you’re wondering if buyers are still out there, know that there are still people who are searching for a home to buy today. And your house may be exactly what they’re looking for.

3. Can I Afford To Buy My Next Home?

If current market conditions have you worried about how you’ll afford your next move, consider this: you may have more equity in your current home than you realize.

Homeowners have gained significant equity over the past few years, and that equity can make a big difference in the affordability equation, especially with higher mortgage rates than last year. According to Mark Fleming, Chief Economist at First American:

“. . . homeowners, in aggregate, have historically high levels of home equity. For some of those equity-rich homeowners, that means moving and taking on a higher mortgage rate isn’t a huge deal—especially if they are moving to a more affordable city.”

Bottom Line

If you’re considering selling your house in Rhode Island this season, let’s connect, so you have the expert insights you need to make the best possible move today. With five listings hitting in the next two months, I can attest to the market’s vitality!

What’s Ahead for Mortgage Rates and Home Prices?

What’s Ahead for Mortgage Rates and Home Prices?

Now that the end of 2022 is within sight, you may be wondering what’s going to happen in the housing market next year and what that may mean if you’re thinking about buying a home. Many of my RI buyers have been seeking my input on what Q4 and Q1 and Q2 may look like next year. Here’s a look at the latest expert insights on mortgage rates and home prices so you can make your best move possible.

Mortgage Rates Will Continue To Respond to Inflation

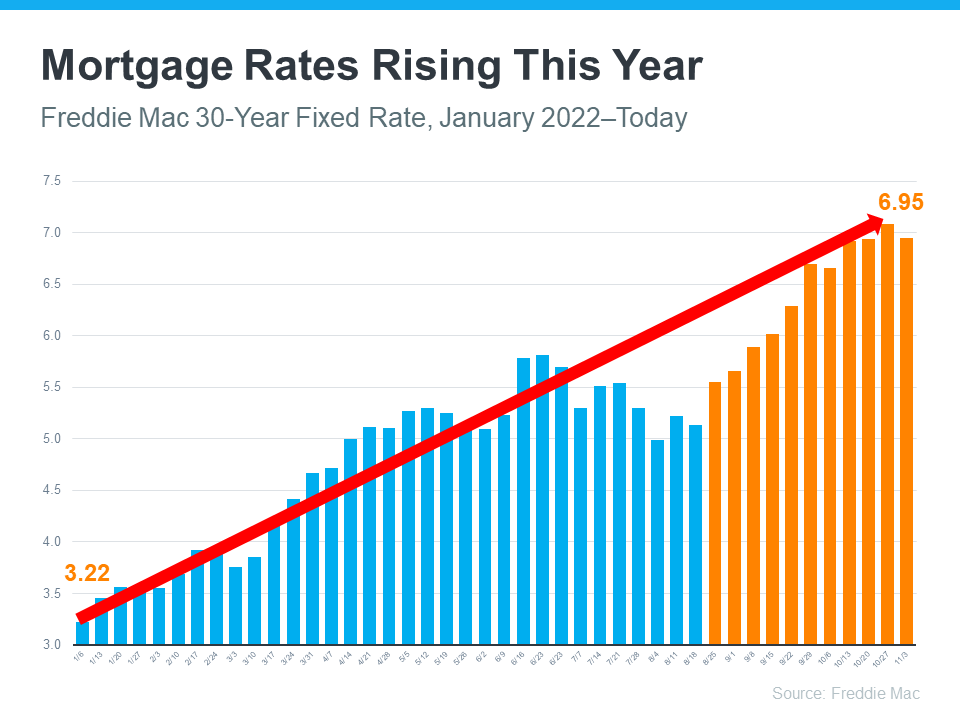

There’s no doubt mortgage rates have skyrocketed this year as the market responded to high inflation. The increases we’ve seen were fast and dramatic, and the average 30-year fixed mortgage rate even surpassed 7% at the end of last month. It’s the first time they’ve risen this high in over 20 years (see graph below):

In their latest quarterly report, Freddie Mac explains just how fast the climb in rates has been:

“Just one year ago, rates were under 3%. This means that while mortgage rates are not as high as they were in the 80’s, they have more than doubled in the past year. Mortgage rates have never doubled in a year before.”

Because we’re in unprecedented territory, it’s hard to say with certainty where mortgage rates will go from here. Projecting the future of mortgage rates is far from an exact science, but experts do agree that, moving forward, mortgage rates will continue to respond to inflation. If inflation stays high, mortgage rates likely will too.

Home Price Changes Will Vary by Market

As buyer demand has eased this year in response to those higher mortgage rates, home prices have moderated in many markets too. In terms of the forecast for next year, expert projections are mixed. The consensus is home price appreciation will vary by local market, with more significant changes happening in overheated areas. As Mark Fleming, Chief Economist at First American, says:

“House price appreciation has slowed in all 50 markets we track, but the deceleration is generally more dramatic in areas that experienced the strongest peak appreciation rates.”

Basically, some areas may still see slight price growth while others may see slight price declines. It all depends on other factors at play in that local market, like the balance between supply and demand. This may be why experts are divided on their latest national forecasts (see graph below):

Bottom Line

If you want to know what’s happening with home prices or mortgage rates, let’s connect so you have the latest on what experts say and what that means for our area. I study the macro and micro real estate markets closely and LOVE sharing my insight with my clients.

Buyers Are Regaining Some of Their Negotiation Power in Today’s Housing Market

If you’re considering buying a home today, there’s welcome news. Even though it’s still a sellers’ market, it’s a more moderate sellers’ market than last year. And the days of feeling like you may need to waive contingencies or pay drastically over the asking price to get your offer considered may be coming to a close.

Today, you should have less competition and more negotiating power as a buyer. That’s because the intensity of buyer demand and bidding wars is easing this year. So, if bidding wars were the biggest factor that had you sitting on the sidelines, here are two trends that may be just what you need to re-enter the market.

1. The Return of Contingencies

Over the last two years, more buyers have been willing to skip important steps in the home buying process, like the appraisal or inspection, to try to win a bidding war. But now, fewer people are waiving the inspection and appraisal.

The latest data from the National Association of Realtors (NAR) shows the percentage of buyers waiving their home inspection and appraisal is declining. And a recent survey from realtor.com confirms more sellers are accepting offers that include these conditions today. According to their August study:

- 95% of sellers reported buyers requested a home inspection

- 67% of sellers negotiated with buyers on repairs as a result of the inspection findings

This shows buyers are more able to include these conditions in their offers today and negotiate as needed based on the inspection outcome.

2. Sellers Are More Willing To Help with Closing Costs

Generally, closing costs range between 2% and 5% of the purchase price for the home. Before the pandemic, sellers used a common negotiation tactic to cover some of the buyer’s closing costs to sweeten the deal. This didn’t happen as much during the peak buyer frenzy over the past two years.

Today, as the market shifts and demand slows, data from realtor.com suggests this is making a comeback. A recent article shows 32% of sellers paid some or all of their buyer’s closing costs. This may be a negotiation tool you’ll see as you purchase a home. Just keep in mind that limits on closing cost credits are set by your lender and can vary by state and loan type. Work closely with your loan advisor to understand how much a seller can contribute to closing costs in your area.

Bottom Line

Regardless of the extremely competitive housing market of the past several years, today’s data suggests negotiations are starting to come back on the table. This is good news if you’re planning to enter the housing market. Let’s connect to find out how the market is shifting in RI!

What Would a Recession Mean for the Housing Market?

According to a recent survey from the Wall Street Journal, the percentage of economists who believe we’ll see a recession in the next 12 months is growing. When surveyed in July 2021, only 12% of economists consulted thought there’d be a recession by now. But this July, when polled, 49% believe we will see a recession in the coming 12 months.

And as more recession talk fills the air, one concern many people have is: should I delay my homeownership plans if there’s a recession?

Here’s a look at historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession would mean for the housing market today.

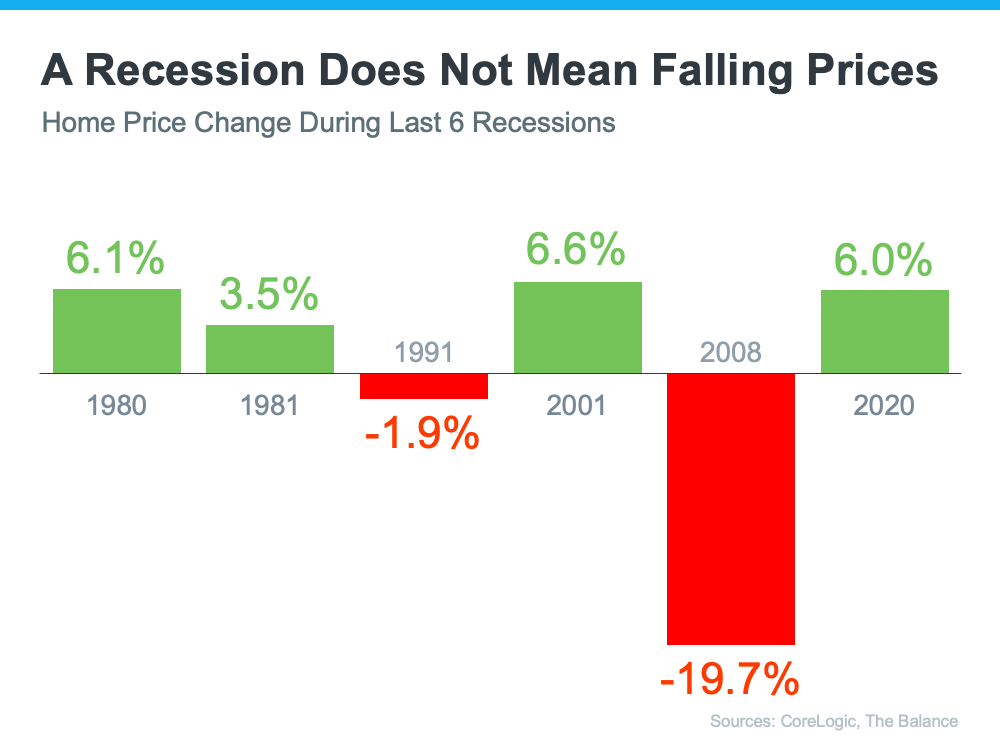

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at the recessions going all the way back to 1980, home prices appreciated in four of the last six recessions. So, historically, when the economy slows down, it doesn’t mean home values will fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would repeat what happened then. But this housing market isn’t about to crash. The fundamentals are very different today than they were in 2008. So, don’t assume we’re heading down the same path.

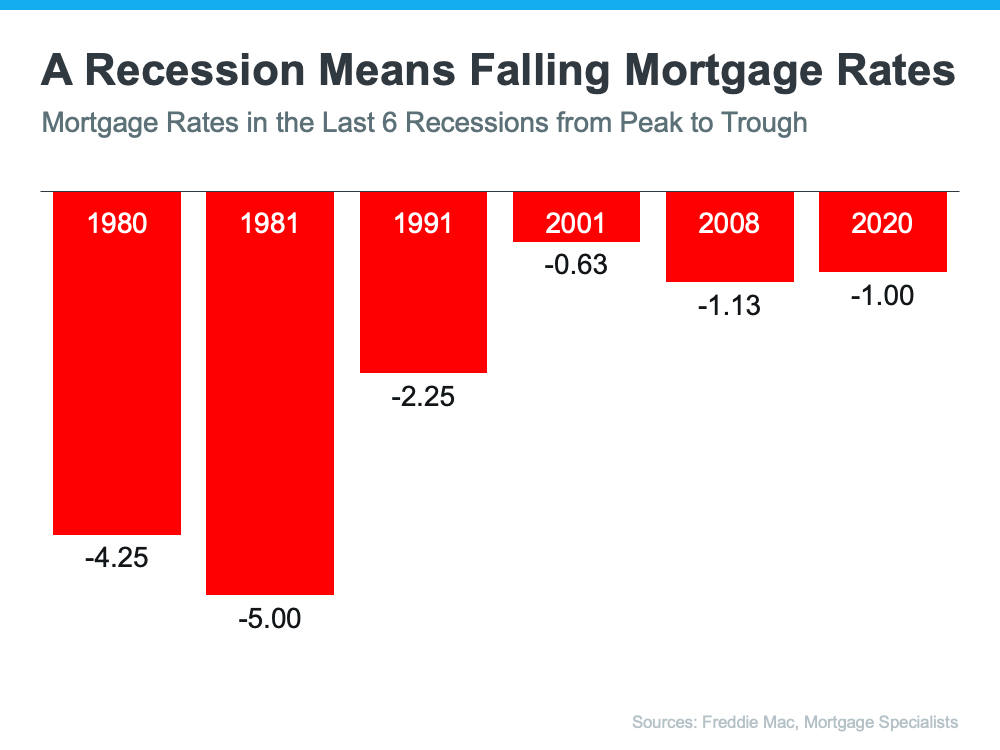

A Recession Means Falling Mortgage Rates

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the chart below shows, historically, each time the economy slowed down, mortgage rates decreased.

Fortune explains that mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

And while history doesn’t always repeat itself, we can learn from and find comfort in the historical data.

Bottom Line

There’s no doubt everyone remembers what happened in the housing market in 2008. But you don’t need to fear the word recession if you’re planning to buy or sell a home. According to historical data, home price gains have stayed strong in most recessions, and mortgage rates have declined. In fact , sale prices for the month of July were up 7.3 % over this time last year and list prices are up 10%

If you’re thinking about buying or selling a home, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals. I am here to help!