Signs of Improved Homebuyer Affordability This Fall

While affordability has been a major challenge in recent years, encouraging trends are starting to emerge — and they’re making the dream of homeownership a bit more attainable for many.

Here are the 3 reasons affordability is showing signs of improvement this fall:

-

Mortgage Rates Have Eased Slightly

Even a small dip in rates can mean hundreds of dollars in savings on monthly payments. Buyers in Rhode Island and Southeastern Massachusetts are already feeling that difference. -

Home Price Growth Has Slowed

After years of steep increases, home prices in our region are showing more balanced growth — giving buyers more breathing room and helping sellers set strategic, competitive prices. -

Wages Are Rising

With incomes ticking up, buyers have a bit more power to keep pace with costs, helping to narrow the affordability gap.

What This Means for RI & Southeastern MA Buyers and Sellers

In towns across Rhode Island and nearby Massachusetts — from Barrington to Providence to Seekonk — these shifts mean opportunity. Buyers may find their budgets stretch further than they did earlier in 2025, and sellers can benefit from listing while buyer confidence strengthens.

👉 Want to dig deeper into these trends?

Click the link below to read the full article and see why this fall may be the right time to make your move:

Read the full article here » https://www.simplifyingthemarket.com/en/2025/09/22/3-reasons-affordability-is-showing-signs-of-improvement-this-fall?a=535214-8638ba58f9b6348ae340b116d7982127

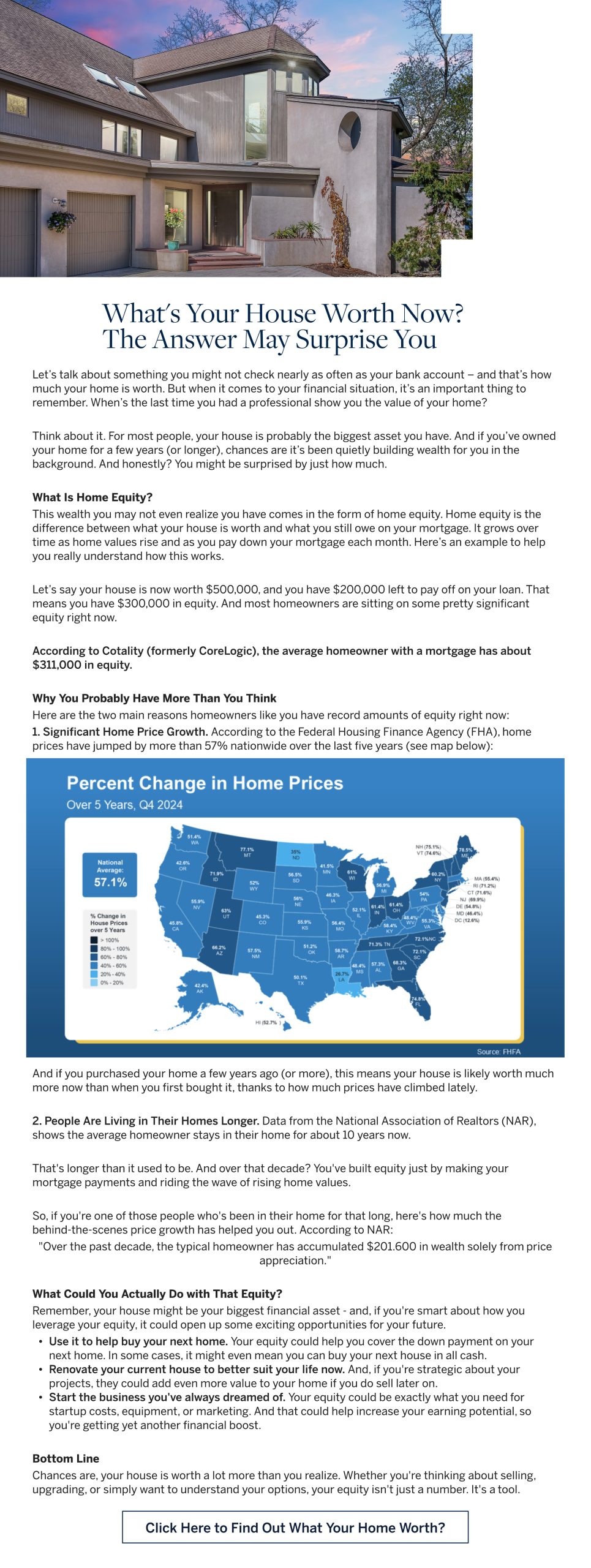

As we move through 2025, Rhode Island’s housing market continues to make waves with persistent price gains, strong buyer demand, and slowly increasing—but still constrained—inventory. The latest report from the Rhode Island Association of Realtors places the median single-family home price at $520,000 in June, reflecting a 5.3% year‑over‑year increase, and a remarkable 73.6% increase since 2019 rirealtors.org+1rhodeislandliving.com+1. Meanwhile, total listings remain low: with only about 2–2.5 months of supply, it’s well below the 5–6‑month threshold considered balanced rirealtors.org+1Houzeo+1.

Comparatively, Redfin reports a median sale price of $533,800 in June, up 2.3% from the previous year, with home sales increasing nearly 13% YoY and inventory up roughly 7.8% Redfin. Zillow’s data shows average home values around $495,600, up 4.3%, with homes selling in approximately 10 days on average Houzeo+2Zillow+2Architectural Digest+2.

In the first quarter (Q1) of 2025, RI saw fewer single-family transactions (‑3.2% YoY), but prices climbed to $465,000, up from $440,000—a 5.7% increase. Condominiums rose 14% to a median of $390,000, and multifamily homes posted a 12% jump to $570,000 rirealtors.org+1rhodeislandliving.com+1.

On the national stage, Zillow has named Providence among the “Top 10 hottest housing markets for 2025”, driven by strong demand, limited supply, and its appeal as relatively affordable compared to larger metros like Boston or New YorkArchitectural Digest.

🏠 What This Means for Buyers, Sellers — and Where Prices May Be Headed

-

Sellers remain in a strong position: low inventory and rising prices mean homes often sell quickly and sometimes above list price. Redfin data shows over 52% of Rhode Island homes sold above list price in June, and the average sale‑to‑list ratio hovered around 101.3% Zillow+2Redfin+2Houzeo+2.

-

Buyers face competition—but there’s cautious optimism. While some sellers engage in bidding wars, areas with price drops and higher days on market may offer negotiation chances.

-

Price Forecast: National forecasts suggest strong appreciation continues. A recent HireAHelper/Redfin analysis projects that by 2030, Rhode Island’s median home price could approach $855,000, potentially requiring average incomes near $190,000 just to remain affordable Houzeonypost.com.

Curious how these state‑level trends compare with what’s projected for the rest of 2025? Read on to dive into the forecast article below — plus what it all means for your next move in the Ocean State market.

The market is shifting, and the sharpest homeowners I know are staying ahead of it – even if they aren’t ready to sell today. Because being informed now means being prepared later.

Here’s what I’m seeing that you need to know:

Right now, 1 in 5 homes on the market are lowering their asking price.

But the homes that are selling? They’re priced right with what today’s buyers are actually looking for, and willing to pay.

Getting that dialed in the first time takes more than guesswork. It takes strategy, timing, expertise, and a clear understanding of what’s really happening in our area. That’s the reality – and it’s where I help my clients win.

Because home values are up 55% over the last 5 years, so you have room to move and still come out ahead.

Here’s a short blog I put together for you that sums it all up:

What Every Homeowner Needs to Know in Today’s Shifting Market

Even if you’re not ready to sell, but you just want to know what’s impacting your home, let’s have a quick conversation.

I’ll share my expert opinion based upon facts and show you exactly what’s taking place in our local market. That way, you can decide what makes the most sense for you – now or later. No strings attached.

Best,

Sarah Huard

(401) 255-2578

sarah.huard@mottandchace.com

If you have a mortgage rate around 3%, chances are you’ve wrestled with the idea of moving—only to feel stuck because of that ultra-low rate. After all, why give that up? It’s a logical concern in today’s market.

But here’s a more powerful question to ask: Will you still be living in your current home five years from now?

Let’s flip the script. People don’t usually move because of their mortgage rate—they move because life changes. Whether it’s a growing family, a new job, retirement, or simply the desire for a better layout or location, most moves are driven by personal needs, not interest rates.

Here’s What To Consider:

1. Life Comes First

Do you see any changes on the horizon? Are your kids moving out soon? Are you craving more space, less maintenance, or a home office? If your home no longer fits your life, staying put may not be the best option—no matter the rate on your current mortgage.

2. Time Has a Cost

Even a delay of one or two years can mean a big difference in your future home’s cost. The housing market continues to evolve—and home prices are projected to rise steadily for the next several years.

3. What the Experts Are Saying

Fannie Mae surveys over 100 housing experts quarterly, and the consensus is clear: home prices are expected to continue increasing through 2029. That means the longer you wait, the more you may pay down the line.

4. Your Mortgage Rate Isn’t Everything

A low rate doesn’t help much if your home no longer suits your needs. Yes, today’s mortgage rates are higher—but there are creative financing options, negotiation strategies, and long-term plans that can make a move not only possible, but smart.

5. You Don’t Have To Figure It Out Alone

As a local real estate expert, I’m here to help you explore your options. Whether you’re ready to move now or just starting to think about the future, let’s talk about what’s best for you—not just financially, but for the life you’re building.

Ready to chat about your timeline and explore what a smart move could look like?

Reach out anytime—I’m here to help you think through every angle and guide you every step of the way.

Sarah Huard, Mott & Chace Sotheby’s International Realty

Serving Rhode Island and Southeastern Massachusetts with strategy, hustle, and heart.

Click on the link below for more reasons why moving now may be in your best interest!

Lately, it feels like a lot of people have been asking the same question: “Is the housing market about to crash?”

If you’ve been scrolling through social media or watching the news, you might have seen some pretty scary headlines yourself. That’s why it’s no surprise that, according to data from Clever Real Estate, 70% of Americans are worried about a housing crash in 2025.

But before you hit pause on your plans to buy or sell a home, take a deep breath. The truth is: the housing market isn’t about to crash – it’s just shifting. And that shift actually works in your favor.

Today’s Inventory Keeps the Housing Market from Crashing

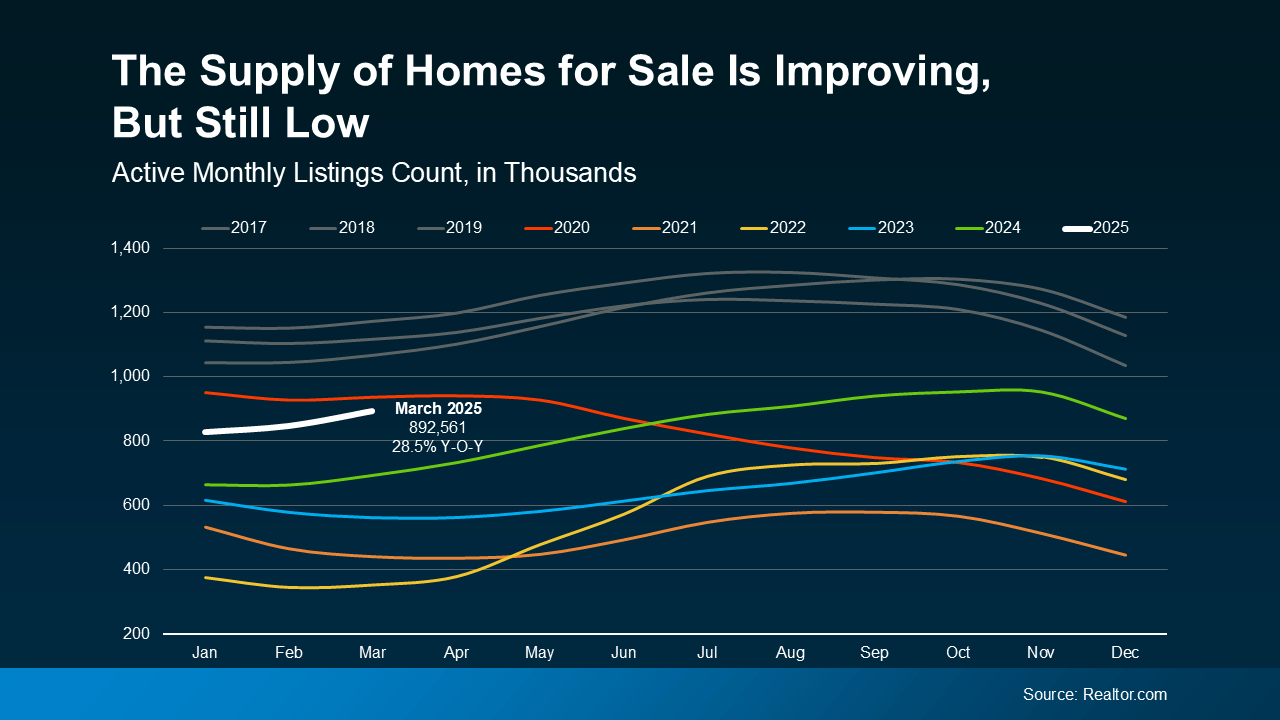

Mark Fleming, Chief Economist at First American, says:

“There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.”

Think about it. If there’s a shortage of something – like tickets to a popular concert – prices go up. That’s what’s been happening with homes. We still have a shortage of supply. Too many buyers and not enough homes push prices higher.

Check out the white line for 2025 in the graph below. Even though the number of homes for sale is climbing, data from Realtor.com shows we’re still well below normal levels (shown in gray):

That ongoing low supply is what’s stopping home prices from dropping at the national level. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

That ongoing low supply is what’s stopping home prices from dropping at the national level. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“… if there’s a shortage, prices simply cannot crash.”

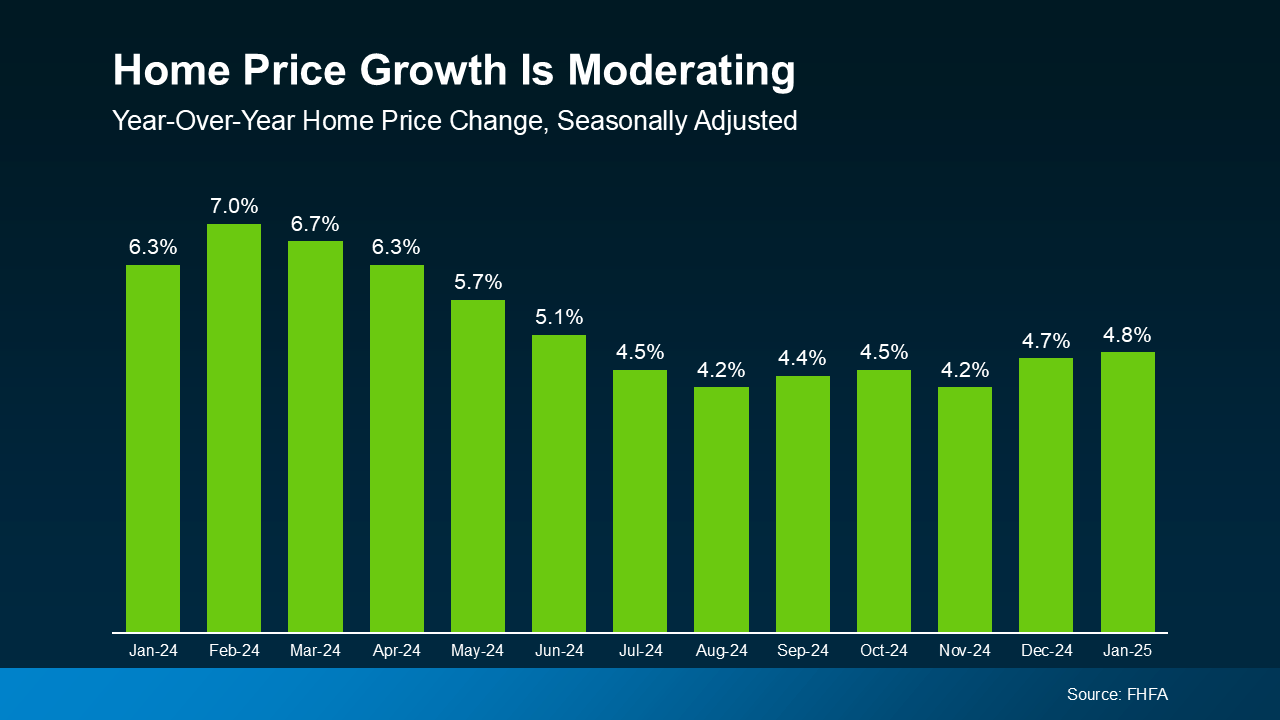

More Homes for Sale Means Price Growth Is Easing

And, as more homes become available, that takes some of the intense upward pressure off home price growth – leading to healthier price appreciation.

So, while prices aren’t falling nationally, growing inventory means they also aren’t rising as fast as they were. What we’re seeing is price moderation (see graph below):

And according to Freddie Mac, that moderation should continue through the rest of this year:

And according to Freddie Mac, that moderation should continue through the rest of this year:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

Put simply, that means prices will continue going up in most areas, just not as quickly. That’s good news for anyone who’s been having trouble finding a home and feeling sticker shock from the rapid price appreciation of the past few years.

But of course, what’s happening with prices and inventory is going to vary by local market. So, here’s the scoop on what is happening in RI!

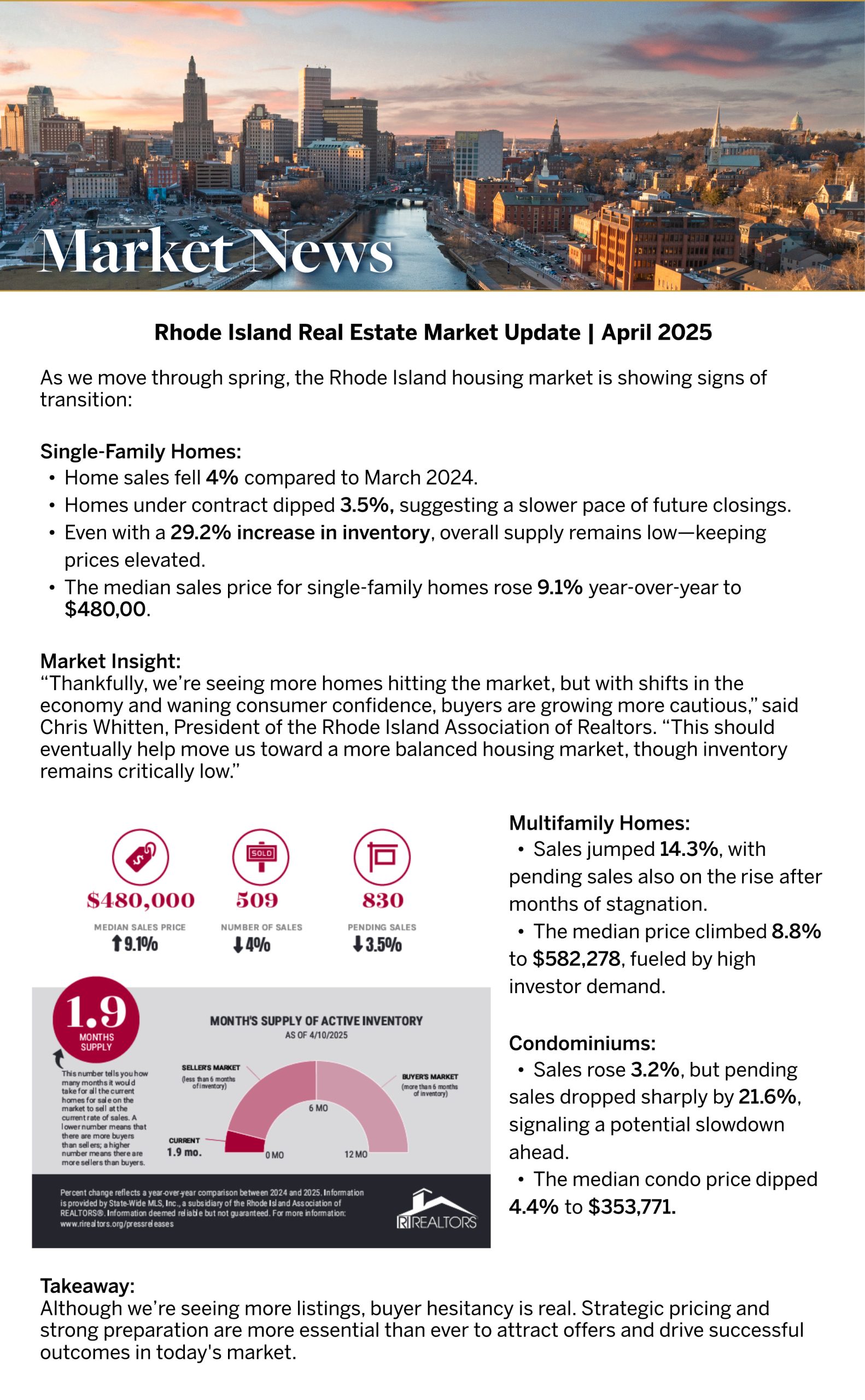

In Rhode Island, March’s median sold price reached $480,000, with inventory still tight at just 1.7 months—a far cry from the 6 months that signals a balanced market. Translation? Buyer demand remains high, and values are holding strong.

More listings mean more choice for buyers, which slows down how quickly prices rise—but prices are still rising. It’s not decline—it’s healthy growth. 💪🏼

So… how does this shift affect your game plan?

Let’s strategize your next move—whether buying or selling, I’ve got you.

Bottom Line

So… how does this shift affect your game plan?

Let’s strategize your next move—whether buying or selling, I’ve got you.

Don’t let the talk scare you. Experts agree that a housing market crash is unlikely in 2025. As Business Insider reports:

“. . . economists who study housing market conditions generally do not expect a crash in 2025 or beyondunless the economic outlook changes.”

Instead, we’re heading into a housing market that’s healthier and more balanced, with slower price growth and more opportunity.

Let’s chat about what’s happening in our local market and how you can make the most of it.

I sell throughout the state of Rhode Island and cover Southern Massachusetts!

One big mistake you must avoid when selling your house this year is setting your price too high. It might seem like overpricing gives you room to negotiate or could really boost your profit, but the reality is that it usually backfires.

Realtor.com says almost 20% of sellers — that’s one in five — have to reduce their price to get their house sold. And you don’t want to be one of them. Here’s why starting too high can lead to trouble and how to avoid it.

Overpricing Pushes Buyers Away

With mortgage rates and home prices where they are right now, buyers are already stretching their budgets to make a move. So, when they see a house priced too high, they do not think, “I can negotiate.” They’re more likely to think “next” and skip over your house entirely. An article from the National Association of Realtors (NAR) explains:

“Some sellers are pricing their homes higher than ever just because they can, but this may drive away serious buyers . . .”

And if they skip over your listing, you’ll miss out on getting them through the door. That’s the last thing you want because fewer showings mean fewer chances to receive an offer.

The Longer Your House Sits, the More Skeptical Buyers Will Get

Here’s the other issue. An overpriced house tends to sit on the market longer. And the longer a house lingers, the more buyers wonder what’s wrong with it. Is there a problem with the house itself? Are you difficult to work with? Even if the only issue is the price, that extra time creates doubt. As U.S. News says:

“. . . setting an unrealistically high price with the idea that you can come down later doesn’t work in real estate . . . A home that’s overpriced in the beginning tends to stay on the market longer, even after the price is cut, because buyers think there must be something wrong with it.”

At that point, you’ll have no choice but to lower your price to drum up interest. However, that price reduction has its own downside: buyers may see it as another red flag: an issue with the house.

The Key To Finding the Right Price for Your House

So, what’s the secret to avoiding all these headaches? It’s simple. Work with a local real estate agent who knows the market and will be honest with you about how you should price your house.

You don’t want to partner with someone who agrees to whatever number you throw out there. That’s not an expert who will get you the best results.

You want an agent who recommends a price based on their expertise. The right agent will use real-time data from your local market to help you land a price that makes sense — one that grabs attention, attracts buyers, and still enables you to walk away with a great return. Someone who has been there and done that – and done it well. That’s the agent you want to work with.

Bottom Line

Remember, if the price isn’t compelling, it’s not selling. Instead of shooting too high and scaring off buyers, work with a local agent who can price it right.

Let’s team up and make sure your house hits the market with the right price, gets noticed, and gets sold. I pride myself on delivering an unmatched work ethic, tireless grit, fierce client loyalty, and a results-driven, hands-on agency to each client I “get” to represent!

Click on the link below for the downlow on why buying now may be the way to go!

Copyright © 2024 Mott & Chace Sotheby’s International Realty. All rights reserved. Sotheby’s International Realty® and the Sotheby’s International Realty Logo are service marks licensed to Sotheby’s International Realty Affiliates LLC and used with permission. Mott & Chace Sotheby’s International Realty fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each franchise is independently owned and operated. Any services or products provided by independently owned and operated franchisees are not provided by, affiliated with or related to Sotheby’s International Realty Affiliates LLC nor any of its affiliated companies. The updated disclaimer above is to be utilized for consumer-facing materials created by affiliate Mott & Chace Sotheby’s International Realty, including a local affiliate Mott & Chace Sotheby’s International Realty website. All rights reserved.